The early months of the coronavirus pandemic saw the U.S. economy plunge at its fastest rate in history. Over a two-month period, the jobless rate shot up from 3.5% in February 2020 to 14.7% in April—its highest level since 1940—while second quarter GDP declined 32.9% on an annualized basis. During this period the Congressional Budget Office forecast that the unemployment rate would remain above double-digits for more than six quarters, ending 2021 at 10.1%. All signs pointed to the U.S. sinking into the worst downturn since the Great Depression, or maybe even into another depression.

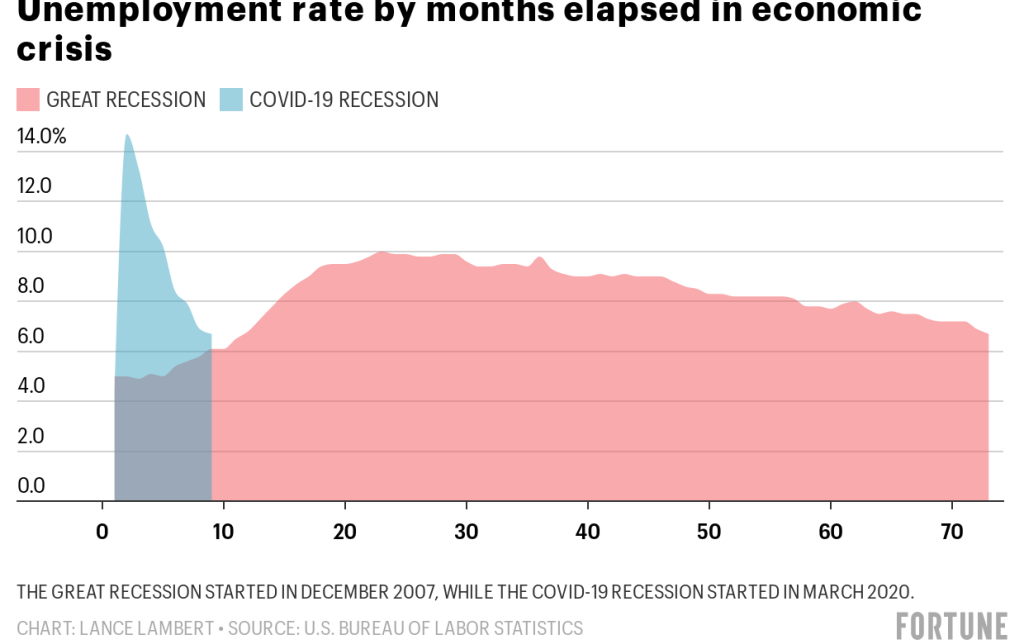

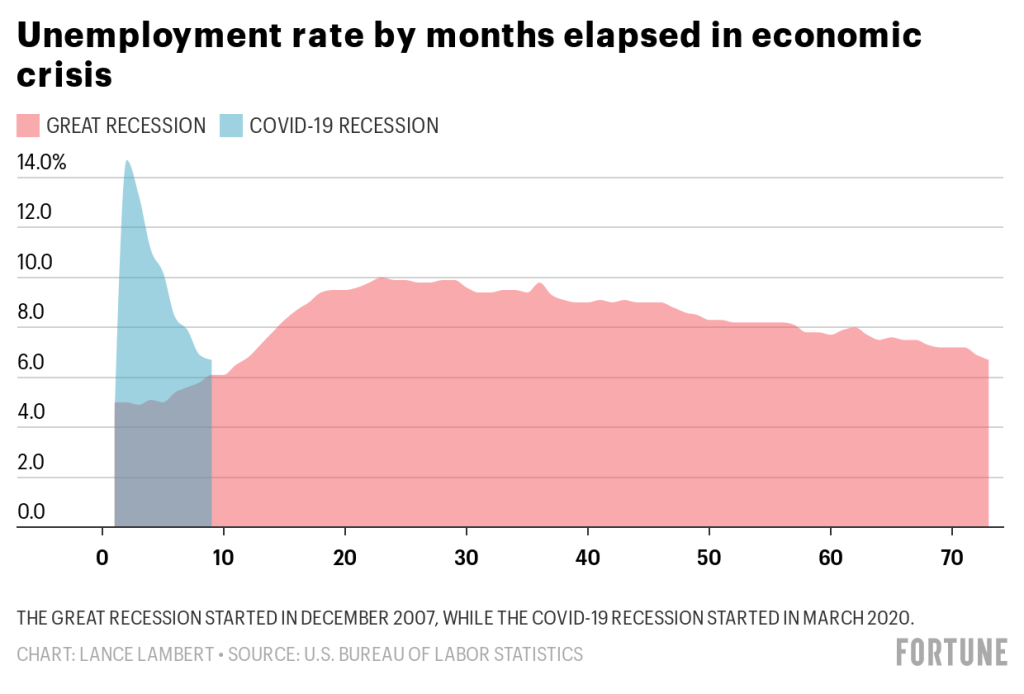

But the bleakest outlooks didn’t come to pass. Despite a lingering pandemic and mass joblessness, the recent economic recovery on paper is among the fastest in American history—at least on paper. Since peaking in April, the unemployment rate has fallen every month, and it now sits at 6.7%. During this crisis the unemployment rate was above 7% for six months. For comparison, the Great Recession that followed the financial crisis saw unemployment top 7% for 59 consecutive months, from December 2008 to October 2013. That means that after the Great Recession, the economy took almost 10 times as long as it did in what we’ll call the COVID-19 Recession to bring the jobless rate under 7%. [See the chart below.]

“We view the coronavirus recession as much more V-shaped than previous postwar cycles, which were mostly driven by financial shocks to asset markets and income,” wrote Goldman Sachs researchers in a November 2020 report. During financial crashes, like the one in 2008, lending dries up and businesses struggle to borrow: Cue slow growth. Fortunately, that hasn’t been an issue during this recent downturn.

This doesn’t mean the current economy is strong, or that we’re close to a full recovery. Look no further than the fact 10.7 million Americans are jobless and looking for work. While the country looks to have avoided the darkest scenario of a multi-year depression, full economic healing is still some distance away.

In part, the economy recovered so quickly during the spring and summer because so many of the job cuts that occurred during the spring lockdowns were temporary. Employers like barber shops and dental offices that furloughed or cut workers during the onset of shutdowns were able to bring those workers back once their states eased up on restrictions. In June 2020 alone, 4.8 million workers were hired or rehired. But those easy job recoveries dried up months ago, and as a result the economic rebound is slowing. In November, the economy added just 245,000 jobs, enough to push the jobless rate down from 6.9% to 6.7%.

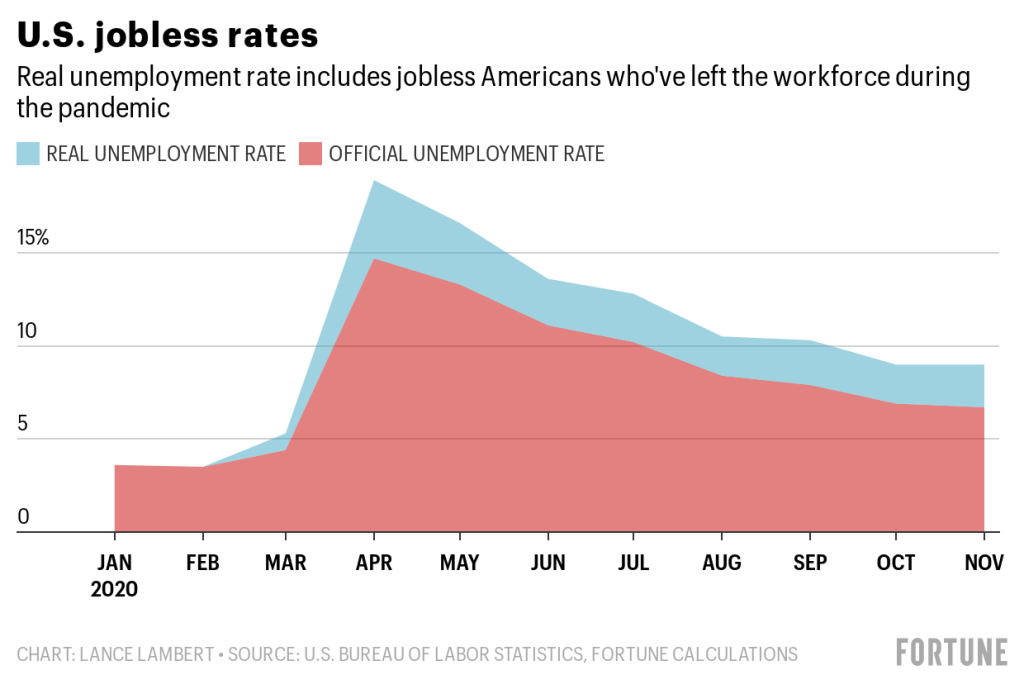

The sustained drop in the unemployment rate signals a growing economy. However, that figure is also severely undercounting joblessness. The Bureau of Labor Statistics (BLS) official unemployment rate calculation only includes as “unemployed” out-of-work Americans who are searching for new positions. If jobless persons aren’t searching, they get dropped out of the civilian labor force statistics altogether. (The unemployment rate is calculated by dividing the number of unemployed Americans by the civilian labor force count).

That method of calculation makes the unemployment rate ill-suited for measuring periods when masses of workers drop out of the labor force. That’s exactly what occurred during the first months deadly pandemic. Health concerns have led some workers, including many senior citizens and immunocompromised Americans, to quit looking for work until the virus is tamed. Meanwhile, many parents—usually moms—were forced to stop working in order to attend to school-age kids whose schools are remote or hybrid. That’s why the civilian labor force declined from 164.5 million in February 2020 to 156.5 million in April 2020. It has since rebounded to 160.5 million, but is still down 4 million from pre-crisis levels.

If the BLS were to include those 4 million jobless Americans who’ve yet to return to the workforce in its unemployment rate, the “real” jobless rate would sit at 9% for November. That’s well above the current 6.7% rate. Still, even this real unemployment rate is falling: It peaked at 18.9% in April, when the official unemployment rate was at 14.7%.

Regardless of how one measures the U.S. economy, the trend shows that the country is growing while also seeing its rate of growth slow. In the third quarter of 2020, from July to September, GDP climbed 33.1% on an annualized basis. But we aren’t maintaining that rate. Goldman Sachs expects the upcoming release of 2020 fourth quarter GDP growth to show an economy that grew by 5%.

Why is growth slowing? Economists point to the ongoing pandemic, which keeps businesses like airlines and hotels constrained and prevents a full economic rebound. That’s why a successful vaccine rollout is so critical.

“In the U.S., we expect virus resurgence to weigh on activity through January, though services activity has proven more resilient than expected. We expect a large rebound in first half of 2021 on the back of widespread immunization—with 50% of the population expected to be vaccinated by April—and forecast above-consensus 5.3% growth in 2021,” Goldman Sachs researchers wrote in a December report.

In that scenario, Goldman Sachs forecast a jobless rate of 5.2% by the end of 2021. If that comes to fruition, it would mark a historic economic rebound from one of the worst crashes in U.S. history. For comparison, following the 2007-2009 Great Recession, the jobless rate didn’t get back down to 5.2% until July 2015.

More must-read finance coverage from Fortune:

- When to expect $600 checks and $300 enhanced unemployment payments

- A brief history of Bitcoin bubbles

- From Bitcoin to Asian tech stocks, these are the biggest winners and losers of the 2020 global markets

- The biggest business scandals of 2020

- Under Biden, expect more scrutiny of Big Tech and mergers